Wall Street analysts now project artificial intelligence investment will reach $1 trillion by 2027 as major technology companies accelerate their infrastructure spending.

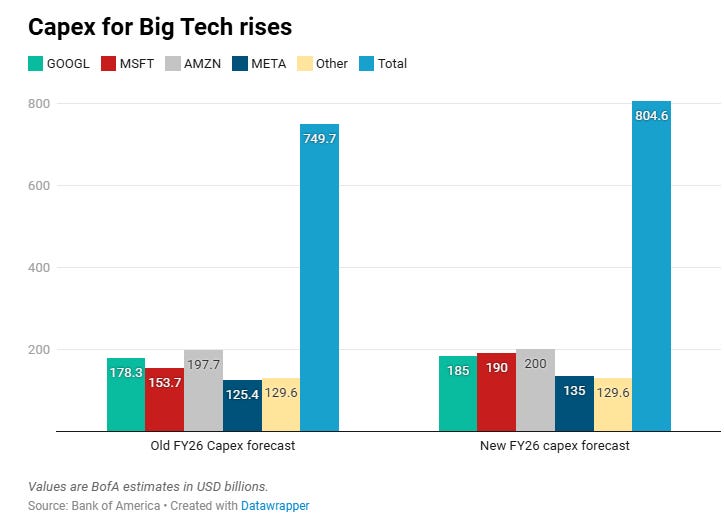

Bank of America data shows Big Tech capital expenditures have been revised upward by nearly 30% so far in 2026, driven by surging demand for AI compute capacity. The spending includes investments in data centers, GPUs, and cloud infrastructure across companies like Microsoft, Google, Amazon, and Meta.

The $1 trillion figure represents only traditional Big Tech players and excludes emerging cloud providers like Oracle, CoreWeave, Crusoe, and xAI. These additional players are building capacity through corporate debt and third-party financing, with Crusoe expected to go public in 2026.

Labor Market Shows Mixed AI Impact

Despite fears of widespread job displacement, AI's employment effects remain ambiguous. Call center employment in the Philippines has grown to nearly two million workers since 2016, continuing through the AI boom.

This reflects Jevons paradox in action: as AI makes customer service interactions cheaper and faster, companies are purchasing more of them rather than fewer. Lower cost per interaction drives expansion into new markets and channels rather than workforce reduction.

Sectors with the highest AI adoption rates have seen the strongest growth in new business applications since 2022, suggesting AI is lowering barriers to company formation. However, major tech corporations continue conducting layoffs to offset AI infrastructure spending.

Infrastructure Investment Accelerates

The acceleration correlates directly with increased demand for inference compute as generative AI applications proliferate. Corporate bonds and venture capital are subsidizing the "tokenmaxxing" trend, where developers maximize AI token usage across applications.

While revenue increases in cloud computing and advertising are legitimizing the capital expenditure surge, the broader economic return on investment remains uncertain. Questions persist about how productivity gains will diffuse through society and impact labor markets.

The spending trajectory suggests continued parabolic growth through 2027, with infrastructure buildout outpacing current revenue justification across the industry.

💬 Discussion

Sign in to join the discussion.

Sign in →No comments yet — be the first.